In April 2026, I went through the x402 ecosystem report: 167 million transactions, $50 million in volume, 480,000 agents. The numbers looked pretty good.

Then I pulled up Artemis's on-chain analysis.

Roughly half was wash trading — the same wallets buying from and selling to themselves. Strip away the noise, and the real daily volume was $28,000. Average transaction: $0.20.

Try to square that with the "trillion-dollar agent economy" narrative, and you get this picture: someone meticulously painting 200 parking spots in an empty lot.

But here's what makes it interesting: Google, Microsoft, and AWS are all building highways to that parking lot. Coinbase's CEO is out there championing it in person. Stripe is plugging its payment stack into it. Meta put serious money on the table to buy an AI social network.

Either they've collectively lost their minds, or they see something the rest of us don't.

What These Companies Are Betting On

Let's get the concept straight. ChatGPT helping you write emails, Copilot auto-completing your code — that's not an AI economy. That's "humans using AI." You give the instructions, AI executes, you make the call, you pay. AI is just a smarter Excel in that chain.

What people mean by an AI-native economy is something different: agents that hold their own assets, discover demand, negotiate, and settle payments — without needing you to sign off at every step. Infrastructure that AI can use directly — that's what counts as the foundation for this economy.

What these giants are scrambling for is the power to define the underlying plumbing. If the agent economy actually takes off, whoever owns the pipes takes everything. Arriving six months late might mean arriving an era late.

Why Blockchain Keeps Coming Up in AI Commerce

A lot of that plumbing is tied to on-chain infrastructure. This isn't purely the crypto community talking to itself — though the echo-chamber component is admittedly high. But if agents are going to operate as independent economic actors, they'll run headfirst into some very real walls in traditional finance.

The identity problem. AI isn't a person, and it's not a legal entity. It can't pass KYC or open a bank account. The entire Stripe and PayPal ecosystem is built on the premise that "you have an ID."

The micropayment problem. The transaction granularity between agents is $0.001 per API call. Nobody is paying a $0.30 Visa processing fee on a tenth-of-a-cent transaction.

The autonomy problem. If every transaction requires "please get human authorization," the agent economy collapses right back into "AI-assisted human economy."

And then there's the real killer: trust is a false premise here. Your agent takes on a data-labeling job, hallucinates halfway through, and the output is garbage. Worse: it gets hit with a prompt injection and sends client data to a third party. Who's responsible? An agent can't go to prison. The existing legal system has no mechanism for handling "a piece of code hallucinated." You can't punish an untrustworthy agent, and deterring its owner isn't much easier.

One solution is to take trust out of human hands and hand it to code. On-chain smart contracts plus staking: agents put up collateral before taking a job; if they botch it, the contract automatically deducts — no subjective human judgment involved.

That said, traditional finance isn't sitting idle. Stripe has already rolled out its Agentic Commerce Suite and Shared Payment Tokens, developed jointly with Visa and Mastercard, letting agents initiate payments within defined boundaries. A human does KYC once and delegates limited payment authority to an agent.

So the more honest assessment is probably this: for AI helping humans buy things — booking flights, renewing SaaS subscriptions — traditional payments work just fine. Crypto's structural advantage is actually quite narrow. Only when transactions are continuous, autonomous, sub-cent, and involve zero human participation does on-chain payment become truly irreplaceable. And that kind of pure machine-to-machine trading barely exists right now.

The two tracks will coexist for a long time. It's not a replacement story.

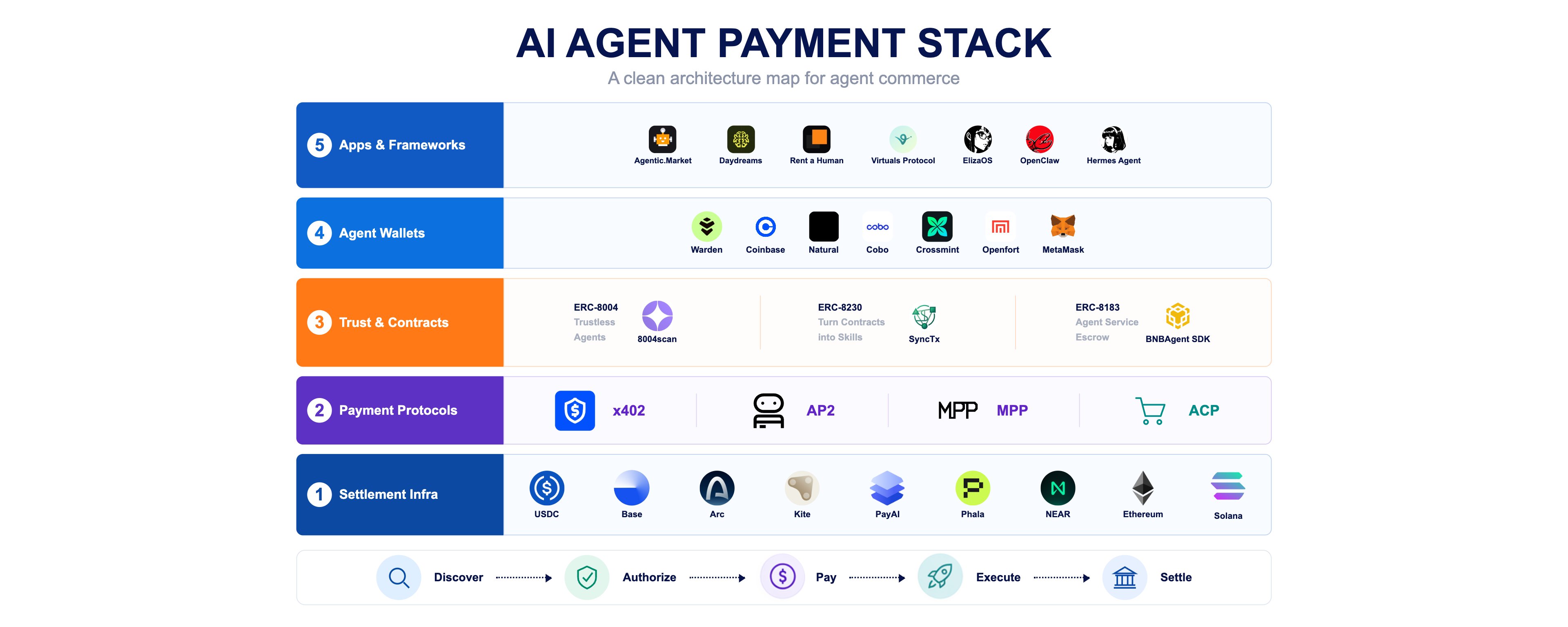

How Far Along Is the Infrastructure

As of April 2026, the crypto track's stack has taken rough shape. From the bottom up:

The settlement layer uses USDC as the de facto base currency. Base (Coinbase's L2) is home turf — 85% of x402 ecosystem transactions settle there.

The payment protocol layer is currently a four-player field.

x402, backed by Coinbase, Cloudflare, and the three major cloud providers, uses HTTP 402 for instant stablecoin payments — agents don't need to apply for API keys. AP2 is Google's authorization framework. MPP, a collaboration between Stripe and Tempo, uses pre-authorization plus streaming micropayments, mixing fiat and stablecoins. ACP is Virtuals Protocol's solution, covering the full agent-to-agent workflow from discovery and negotiation through execution and settlement.

The four protocols aren't mutually exclusive. A single agent system might use three of them simultaneously.

The identity and trust layer is where things get complicated. ERC-8004 went live on the Ethereum mainnet in January 2026, bundling on-chain identity, reputation, and verification together. But there's a catch: can an agent actually trust a contract? It can read the Solidity source code, but it can't verify that the bytecode running on-chain matches the source, and it struggles to spot hidden admin privileges or risks lurking behind an upgrade proxy. ERC-8230 tries to close that gap by having contracts return Markdown-formatted workflow instructions via an instruction() function, embedded in bytecode, immutable — SyncTx built the first production-grade implementation. ERC-8183 takes a different approach: agent service escrow, locking funds and auto-releasing upon completion. All of these standards are still very early. There are no signs of adoption at scale.

On agent wallets, Coinbase Agentic Wallet, Warden, Crossmint, and MetaMask are all building solutions. The technical approaches differ, but the problem they're solving is the same: removing the "human signature required" bottleneck from agent workflows.

The application layer includes Agentic.Market (Coinbase's agent service marketplace, launched April 21), Virtuals Protocol (18,000+ agents, distributing around a million dollars monthly to agents that sell services), and ElizaOS (ai16z's open-source framework). Tools and marketplaces are being built, but right now it looks more like developers demoing to each other. Real external demand hasn't shown up yet.

So where does the traffic come from?

What the First Real Demand Looks Like

With only $28,000 a day in real volume, infrastructure is way ahead of demand. But scrolling through social media discussions, you can pick up some clues.

a16z cited a judgment from Merit Systems' CEO: the first viable model for the agent economy isn't big transactions — it's the compounding effect of microtransactions. $5 buys you 500 one-cent calls — pulling news, checking prices, buying domains, sending emails — and the combined value exceeds $5.

Coinbase product lead Nick Prince noticed something: a third of the people most interested in x402 have zero crypto background. They're AI engineers and SaaS founders with a very specific problem — how to let agents pay for services without applying for API keys. The agent economy's first "commodities" might not be DeFi products at all, but AI developers buying and selling capabilities to each other.

a16z partner Andrew Chen's take is also worth noting: the AI-native killer product won't emerge from "build a platform and wait for them to come." It's more likely to spill out naturally from internal enterprise AI tools. In-house teams are ready-made small networks — no cold start needed.

These three clues point to where demand might sprout, but I'm more interested in a different question: for agents to operate independently, other parties have to trust them first. Arbitration, compliance certification, secure storage, credit scoring — these might be the first things to get priced in the agent economy. In other words, AI's first purchases might be buying trust for itself.

Where Regulators Stand

Three major markets, three different approaches.

The US is fragmented. Law firm Fenwick identified several fault lines: "demonstrable consent" under Regulation E has no definition for AI agents; platforms controlling agent payment flows could trigger MSB (Money Services Business) licensing requirements in various states; agent models that mix fiat and stablecoins fall into a regulatory vacuum. Cryptographic signatures do create audit trails, but as Fenwick also noted, "this code-based authorization has not been tested in court."

The UK is in sandbox mode. The FCA's "AI Live Testing Cohort 2" pulled in Barclays, UBS, and Lloyds, explicitly defining open finance as "the infrastructure layer enabling agentic commerce to scale."

The EU is in legislation mode. MiCA takes full effect in July 2026, requiring audit trails for agent behavior, licensed execution mechanisms, and human override capabilities.

The telling detail: no major regulator is trying to stop this. The disagreement is about how to regulate, not whether to. For the crowd building highways, that counts as good news.

So Are They Actually Crazy?

My read: no, but they're betting very early.

Infrastructure running ahead of applications — this has happened more than once during technological shifts. TCP/IP and the web browser predated e-commerce by years. Today's companies are betting on the same playbook: lay the pipes first, and when the first real use cases break through, ride the growth.

The signals supporting this bet are growing. Regulators aren't trying to kill it — they're figuring out how to manage it. Developers with no crypto background are starting to pay attention to agent payments. Meta put real money behind acquiring Moltbook, an AI social network with 1.6 million agent "users."

But let's be honest: whether this bet pays off hinges on a question nobody can answer yet — what will agents actually trade with each other? The internet's first revenue model at scale was the banner ad, and the people building TCP/IP never saw that coming. What the agent economy's "banner ad moment" will be — nobody knows right now.

April 2026. The AI-native economy is still in its earliest stages. All data and conclusions in this piece require ongoing verification.